Best Shopify Payment & BNPL Apps (2026)

Last updated: April 2026 · Reviewed by the Libautech team, builders of Bundles & Upsell and Shoptank — Built for Shopify apps used by 5,000+ merchants across 50+ countries.

Key Takeaways

- Shop Pay Installments is the zero-friction default for Shopify merchants — powered by Affirm, built into Shopify Payments, no separate integration required, and no extra merchant fees beyond standard processing.

- Klarna, Afterpay, and Affirm are the three dominant BNPL providers in 2026 — each reaches a different customer network, which matters for approval rates on borderline orders.

- BNPL lifts checkout conversion 15–30% on average and raises AOV 20–50% on orders using installments — the single highest-ROI checkout change most Shopify stores can make.

- Merchant fees on BNPL typically run 4–6% per transaction versus 2.9%+30c on credit cards — factor this into margin math before enabling it on low-margin SKUs.

- Sezzle is the strongest alternative for Gen Z and younger millennial customers with the highest approval rates for thin-credit-file shoppers.

- Downpay and SPD cover deposit and split-payment use cases for high-ticket custom, pre-order, or made-to-order products where full upfront payment is a conversion blocker.

Why Payment Flexibility Directly Affects Conversion Rate

Cart abandonment at checkout runs at 70% across e-commerce. The two most cited reasons are unexpected costs and insufficient payment options. Buy Now Pay Later (BNPL) directly addresses the second. Stores that added BNPL options saw checkout conversion rate increases of 15–30% on average, with AOV increases of 20–50% on orders using installment plans.

The BNPL market consolidated significantly between 2022 and 2025. Afterpay was acquired by Block, Klarna went public, and Affirm became the default BNPL provider for Amazon. Shop Pay Installments, powered by Affirm and built natively into Shopify, emerged as the zero-friction option for merchants already on Shopify Payments. The choice between platforms now comes down to market presence, approval rates, and which customers each provider's network reaches.

Payment flexibility is one lever on a broader checkout stack — see our guides to the top social proof apps, best pop-up apps, and best analytics apps to build the full checkout and conversion stack.

This post covers 7 Shopify payment flexibility apps in 2026 — BNPL providers, split payment tools, and deposit platforms — ranked by adoption, checkout conversion impact, and pricing structure.

Quick Comparison: Best Shopify Payment & BNPL Apps (2026)

| App | Rating | Merchant Fee | Model | Primary Markets | Best For |

|---|---|---|---|---|---|

| Shop Pay Installments | ⭐ 4.7 | 0% (Shopify absorbs) | 4 payments or monthly | US | Lowest friction, built into Shopify |

| Klarna | ⭐ 4.6 | ~3.29% + $0.30 | Pay in 4 / Pay Later / Financing | US, EU, AU, CA | European markets, brand recognition |

| Afterpay / Clearpay | ⭐ 4.5 | ~4–6% per transaction | 4 interest-free payments | US, AU, NZ, CA, UK | Younger shoppers, AU/NZ market |

| Affirm | ⭐ 4.2 | ~5–7% per transaction | Monthly installments (3–60 months) | US, CA | High-ticket purchases, longer terms |

| Sezzle | ⭐ 4.5 | ~6% per transaction | 4 payments over 6 weeks | US, CA | Shoppers with limited credit history |

| SPD Split Payment & Deposit | ⭐ 4.8 | From $9.99/mo | Split across payment methods | Global | Multiple payment methods per order |

| Downpay: Deposits Made Simple | ⭐ 4.9 | From $9.99/mo | Custom deposits + balance due later | Global | Pre-orders, custom orders, high-value items |

1. Shop Pay Installments

Best for: US merchants on Shopify Payments who want BNPL with zero merchant fees and no separate app integration.

Shop Pay Installments is built directly into Shopify Payments and powered by Affirm. There is no separate app to install, no additional merchant fee on top of Shopify Payments rates, and the option appears automatically at checkout for eligible US customers. Customers can split purchases between $50 and $17,500 into 4 biweekly interest-free payments, or monthly installments up to 24 months for higher amounts.

Shopify absorbs the financing cost rather than charging merchants a separate BNPL fee. For stores already on Shopify Payments, this is the zero-friction starting point before adding any third-party BNPL provider. The Shop Pay recognition in checkout also carries trust — customers have seen it across millions of Shopify stores.

Where it falls short: US only. Stores with significant international traffic need a separate BNPL solution for non-US customers.

Pricing: No additional merchant fee for stores on Shopify Payments.

2. Klarna

Best for: stores with European customers or those wanting the broadest BNPL option set — pay in 4, pay in 30, and longer-term financing in one provider.

Klarna is the leading BNPL brand in Europe with 150M+ active users and significant market share in Sweden, Germany, and the UK. For stores targeting European customers, Klarna's brand recognition creates checkout trust that other BNPL providers cannot replicate in those markets. In the US, Klarna competes directly with Afterpay and Affirm with a growing user base.

Klarna's product range covers three distinct customer needs: Pay in 4 (4 interest-free installments), Pay in 30 (pay the full amount 30 days later — popular in Europe), and longer-term financing for higher-ticket items. Having all three in one integration reduces the need for multiple BNPL providers.

Where it falls short: merchant fees (~3.29% + $0.30 per transaction) add up at volume. Approval rates can be lower than Afterpay for customers without established Klarna accounts.

Pricing: No monthly fee. ~3.29% + $0.30 per transaction (varies by market).

3. Afterpay / Clearpay

Best for: stores targeting younger shoppers in the US, Australia, New Zealand, and UK where Afterpay has the highest brand recognition.

Afterpay (called Clearpay in the UK and EU) pioneered the 4-payment model — 4 equal payments over 6 weeks, interest-free for the customer. The merchant pays a fee per transaction; the customer pays nothing extra if they pay on time. This model has a simple and trusted consumer proposition that drives adoption.

Afterpay's user base skews younger (18–35) and is particularly strong in Australia where it originated. For stores with US, AU, NZ, or UK customer bases, the Afterpay badge at checkout is recognized and trusted in a way that builds conversion. The Block acquisition brought deeper integration with Cash App Pay, expanding the addressable audience.

Where it falls short: merchant fees of 4–6% per transaction are higher than Klarna and Shop Pay Installments. For high-volume stores where BNPL is used on most orders, those fees accumulate significantly.

Pricing: No monthly fee. ~4–6% per transaction.

4. Affirm

Best for: stores selling high-ticket items ($500+) where customers need financing terms of 3–60 months to make the purchase accessible.

Affirm covers longer-term financing that the 4-payment BNPL model cannot. A customer buying a $2,000 item can choose 12, 18, or 24 monthly payments, making high-ticket purchases accessible in the same way a credit card with a promotional rate would. Affirm is integrated as the underlying provider for Shop Pay Installments, so it also has the broadest US Shopify footprint of any BNPL provider.

For stores selling furniture, electronics, fitness equipment, jewelry, or other high-ticket categories, Affirm's longer financing terms directly enable purchases that customers would not complete with a 4-payment option. Average order values on Affirm-financed transactions are significantly higher than on standard 4-payment BNPL.

Where it falls short: merchant fees of 5–7% per transaction are the highest in this category. Affirm is US and Canada only — no European or Asian market coverage.

Pricing: No monthly fee. ~5–7% per transaction.

5. Sezzle

Best for: US and Canadian stores targeting customers who want BNPL but may not qualify for Klarna, Afterpay, or Affirm due to limited credit history.

Sezzle's credit approval model is more inclusive than most BNPL providers — it is specifically positioned to serve underbanked customers and those building credit history. The 4-payment model over 6 weeks is standard. Customers who pay on time can build a Sezzle credit score that unlocks higher purchase limits over time.

For stores in categories purchased heavily by younger or credit-building customers — gaming, fashion, beauty, fitness — Sezzle approves customers that Afterpay or Klarna might decline, expanding the addressable BNPL audience for that store.

Where it falls short: merchant fees of ~6% are on the higher end. Sezzle's brand recognition is lower than Klarna, Afterpay, and Affirm — it does not carry the same checkout trust signal in markets where it is less known.

Pricing: No monthly fee. ~6% per transaction.

6. SPD Split Payment & Deposit

Best for: stores where customers want to split a single order across two different payment methods — two cards, a card and PayPal, or a gift card and card.

SPD is a different category from the BNPL providers above. It does not offer installment financing — it allows a single order to be paid using multiple payment instruments simultaneously. A customer can put $50 on one credit card and $80 on another, or split between a gift card and PayPal. It also enables group payments: sharing a payment link so multiple people contribute to one order.

For stores where this use case is relevant — corporate gifting, shared household purchases, group orders — SPD is the only Shopify app that handles it properly. At $9.99/mo, it is low-cost relative to the conversion impact on applicable orders.

Where it falls short: this is a niche use case. Most stores will see more conversion lift from a BNPL provider than from split-payment functionality.

Pricing: From $9.99/mo.

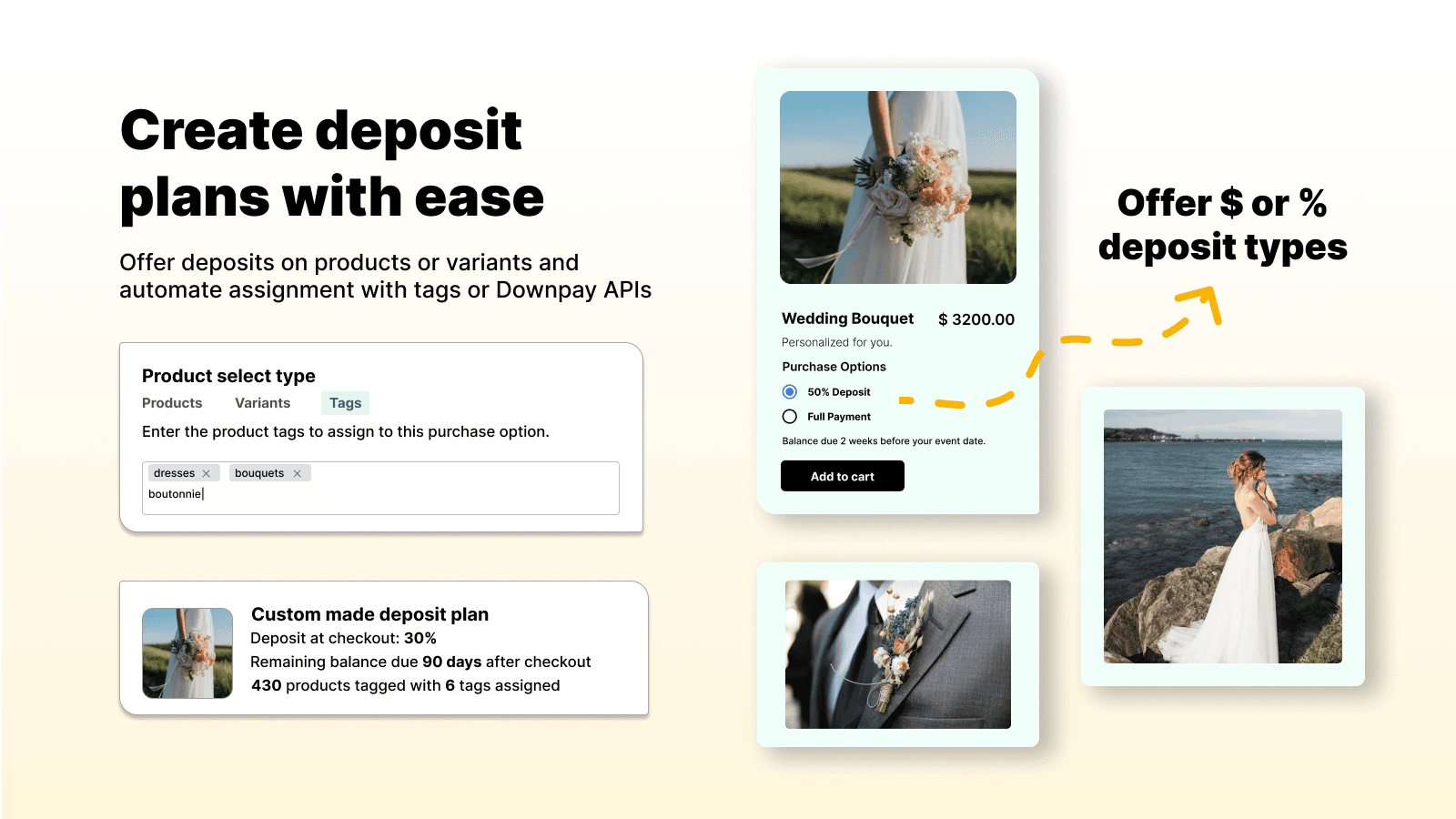

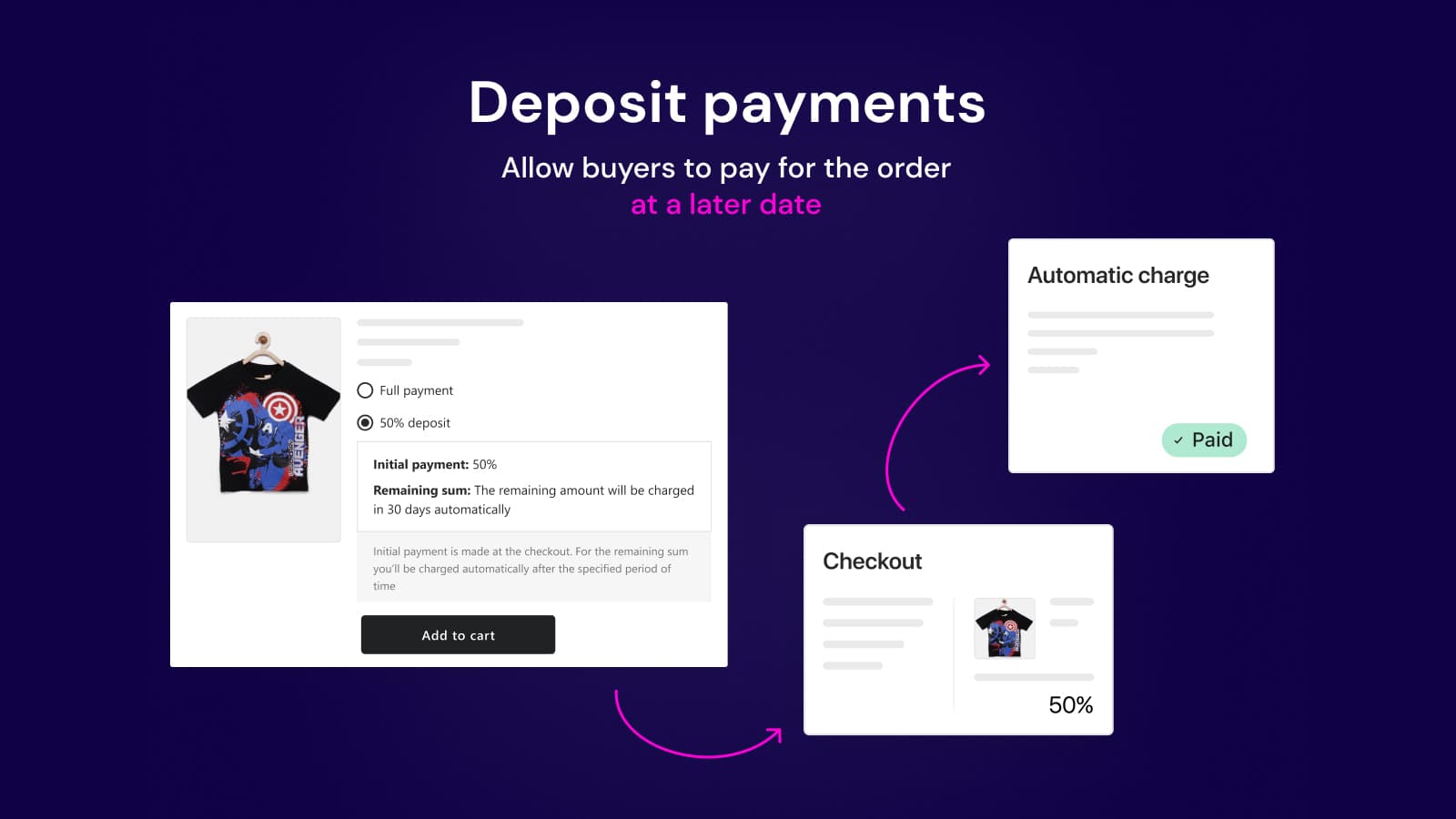

7. Downpay: Deposits Made Simple

Best for: stores selling pre-orders, custom-made, or high-value items that require a deposit upfront and balance collection later.

Downpay handles deposit-based payment workflows. A customer pays a defined percentage (or fixed amount) at order time, and the remaining balance is automatically charged on a future date or when the item ships. This is essential for furniture stores, custom jewellery, made-to-order clothing, and any product with a production lead time where you need to secure commitment before fulfilling.

Shopify Flow integration lets merchants automate the balance-collection trigger based on order status changes — when an order moves to "fulfilled," Downpay can automatically charge the remaining balance. The customer portal allows buyers to update payment methods or cancel before balance collection, reducing support tickets.

Where it falls short: this is specifically a pre-order and deposit tool, not a standard BNPL option. For general purchase financing, the BNPL platforms above are more appropriate.

Pricing: From $9.99/mo.

Which App to Choose

US store on Shopify Payments and want zero friction BNPL immediately: Shop Pay Installments. No separate integration, no additional fee, activates at checkout automatically.

Significant European customer base: Klarna. The brand recognition in European markets is the deciding factor.

Strong AU, NZ, or UK customer base, or targeting younger US shoppers: Afterpay. The brand trust and Cash App Pay integration provide the most recognition in those markets.

Selling high-ticket items ($500+) where monthly financing terms drive AOV: Affirm. The longer-term financing unlocks purchases that 4-payment models cannot.

Pre-orders, custom products, or made-to-order items requiring a deposit: Downpay. Purpose-built for that workflow — nothing else handles it as cleanly.

How We Ranked These Apps

This ranking is based on four criteria applied to every Shopify payment flexibility app tested in 2026. First, Shopify App Store rating and review volume as of April 2026. Second, consumer network reach — a BNPL provider’s value comes partly from how many shoppers already have accounts and recognize the logo at checkout. Third, merchant fees compared against credit card processing, including settlement terms. Fourth, the specific commerce use case each app wins: standard BNPL at checkout, split payments across multiple cards, or deposits on high-ticket and pre-order products.

Payment apps are not mutually exclusive. Most stores running BNPL offer two to three providers simultaneously to maximize approval rates across customer segments. Ratings and review counts reflect the Shopify App Store at the time of our last update and shift as apps release updates.

Frequently Asked Questions

What is the best payment app for Shopify in 2026?

For most Shopify merchants, Shop Pay Installments is the default because it requires zero integration work — it is built into Shopify Payments, powered by Affirm, and adds no extra merchant fee beyond standard Shopify processing. For stores wanting broader BNPL coverage and higher approval rates, adding Klarna and Afterpay alongside Shop Pay Installments captures the full addressable BNPL customer base. The combined setup typically lifts checkout conversion 15–30% compared to card-only checkout.

Klarna vs Afterpay vs Affirm: which is best for Shopify?

All three dominate different customer networks. Klarna is strongest in Europe and increasingly strong in the US, with higher AOV per transaction and three flexible payment structures (Pay in 30, Pay in 4, longer financing). Afterpay (Clearpay in the UK) is the default choice for the US, UK, Canada, Australia, and New Zealand with a highly engaged younger shopper base. Affirm has the strongest financing options for higher-ticket items up to $17,500 and powers Shop Pay Installments natively. Running two or three in parallel maximizes approval rates.

How much does BNPL cost Shopify merchants?

BNPL fees typically range 4–6% per transaction, compared to around 2.9% plus 30 cents for standard credit card processing. Shop Pay Installments on Shopify Payments charges the merchant a similar 4–6% fee depending on the installment plan length. The tradeoff: BNPL transactions typically carry 20–50% higher AOV and 15–30% better checkout conversion, which more than covers the fee gap on most product categories. Low-margin SKUs (under 20% gross margin) should be evaluated carefully.

Does Shop Pay Installments work automatically on Shopify?

Yes for merchants using Shopify Payments in supported countries — Shop Pay Installments is built into the Shopify Payments product and appears at checkout without separate integration work. Merchants need to enable it in Payments settings and accept the terms. For merchants using a different payment processor, Shop Pay Installments is not available and they need standalone BNPL apps like Klarna, Afterpay, or Affirm instead.

What is the difference between BNPL and split payments?

BNPL (Buy Now Pay Later) lets a customer pay over time via a BNPL provider that pays the merchant upfront and collects from the customer in installments — the merchant is not carrying credit risk. Split payments (like SPD) split a single order across multiple cards or payment methods at checkout, paid in full upfront. Deposit apps (like Downpay) charge a partial payment now and the remainder later, typically for pre-orders or custom orders. Each solves a different checkout friction.

Can I offer multiple BNPL options on Shopify?

Yes, and most stores running BNPL offer two to three providers simultaneously to capture the different customer networks. A common stack is Shop Pay Installments (for customers already in the Shop ecosystem), Klarna (for European shoppers and larger orders), and Afterpay (for the younger Australian, UK, and US customer base). Approval rates vary by provider and customer, so running multiple increases the chance that a customer declined by one gets approved by another at checkout.

What Shopify payment apps work best for high-ticket products?

For high-ticket products above $1,000, Affirm is the default because its financing covers orders up to $17,500 across terms from 3 to 48 months. Shop Pay Installments (Affirm-powered) handles the same use case natively within Shopify Payments. For custom or made-to-order high-ticket products where customers hesitate to pay upfront, Downpay for deposits or SPD for split payments solve the conversion blocker directly by reducing the upfront commitment.

Is BNPL available internationally on Shopify?

Yes, but provider availability varies by country. Klarna operates in most European markets, the US, UK, and Australia. Afterpay (as Clearpay) is available in the US, UK, Canada, Australia, and New Zealand. Affirm and Shop Pay Installments are US and Canada focused. Sezzle covers the US and Canada primarily. International stores benefit from stacking region-specific BNPL providers to cover each target market properly.

Do BNPL apps increase Shopify conversion rates?

Yes. Industry data shows BNPL at checkout lifts conversion rates 15–30% on average across e-commerce. The effect is larger on higher-AOV orders (above $100) where upfront payment creates meaningful friction, and on customer segments where credit card access is limited. The AOV lift on BNPL-selected transactions runs 20–50% higher than card-only transactions, because customers feel more comfortable adding items when the per-month cost stays low.

Should I combine payment apps with upsell or bundle apps on Shopify?

Yes — payment flexibility and AOV optimization stack well together. BNPL already raises AOV by 20–50% on its own, and layering an upsell strategy on top compounds the effect. For example, our Bundles & Upsell app drives bundled add-ons before checkout, and when the final total is paid via Shop Pay Installments or Klarna in installments, customers are comfortable with the higher order value because the per-month cost stays manageable. The combination is one of the highest-leverage checkout optimizations available.